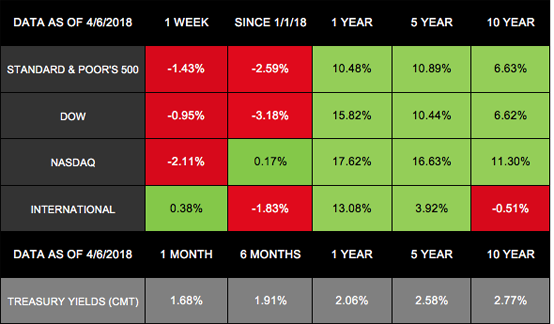

Domestic stocks lost ground last week as trade war concerns continued to rattle investors. With these declines, the Dow officially moved back into correction territory.[1] For the week, the S&P 500 lost 1.43%, the Dow dipped 0.95%, and the NASDAQ dropped 2.11%.[2] International stocks in the MSCI EAFE managed a 0.38% increase.[3]

An escalating trade dispute between the U.S. and China wasn’t the only headline to affect markets. Last week also brought surprising data from the Labor Department. In March, the economy added 103,000 new jobs – far lower than economists anticipated. Meanwhile, wages grew, and unemployment remained a low 4.1%.[4]

We are now 1 week into the 2nd quarter of 2018. As we examine what may lie ahead in the markets, we will also focus on understanding what has happened so far this year. Here are a few key findings from the 1st quarter.

Quarterly Update

In 2017, domestic markets experienced little volatility and significant gains.[5] The 1st quarter of 2018, however, did not continue these trends.

Volatility Returned

The CBOE Volatility Index (VIX), a popular measure of volatility, increased by 81% in Q1, as stock performance fluctuated.

Between January and March, the S&P 500 had 23 days when it lost or gained 1%. In 2017’s last quarter, the index didn’t have a single day where it fluctuated that much. While the return of volatility may feel jarring, it is actually normal. Last year’s calm is what is unusual.[6]

Indexes Had Mixed Results

Major domestic indexes hit new records in January then slipped into corrections the next month. By March’s end, they recovered somewhat from February’s lows, but the S&P 500 and Dow still posted their 1st quarterly losses in more than 2 years. The S&P 500 lost 1.2% and the Dow dropped 2.3%. The NASDAQ ended in positive territory, with a 2.3% gain for the quarter.[7]

The Economy Remained Strong

Despite market volatility and lackluster quarterly performance, the economy appears to be on solid ground. When announcing March’s interest rate increase, the Federal Reserve beefed up the economy’s growth projections and expressed that “the economic outlook has strengthened in recent months.” In 2018, the Fed expects unemployment to fall to 3.8% and the economy to grow by 2.7%.[8]

What’s Ahead

In the coming weeks, we will receive more data that reveals our Q1 economic performance. We will also work to find answers to important questions for the 2nd quarter, such as: What will happen with trade and tariffs? Will the labor market continue to strengthen? In the meantime, if you have questions of your own, we are always here to talk.

ECONOMIC CALENDAR

Tuesday: PPI-FD

Wednesday: Consumer Price Index

Thursday: Jobless Claims, Import and Export Prices

Friday: Consumer Sentiment

[dt_divider style=”thick” /]

[dt_divider style=”thick” /]

Notes: All index returns (except S&P 500) exclude reinvested dividends, and the 5-year and 10-year returns are annualized. The total returns for the S&P 500 assume reinvestment of dividends on the last day of the month. This may account for differences between the index returns published on Morningstar.com and the index returns published elsewhere. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Investment advisory services and insurance services are provided through Absolute Return Solutions Inc., a Registered Investment Advisor.

Any economic and/or performance information cited is historical and not indicative of future results. Absolute Return Solutions Inc. is an investment advisor registered in each state Absolute Return Solutions Inc. maintains client relationships.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indices from Europe, Australia, and Southeast Asia.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

These are the views of Platinum Advisor Strategies, LLC, and not necessarily those of the named representative,

Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

By clicking on these links, you will leave our server, as the links are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] www.cnbc.com/2018/04/06/us-stock-futures-dow-jobs-data-tech-and-politics-on-the-agenda.html

http://performance.morningstar.com/Performance/index-c/performance-return.action?t=@CCO

[3] www.msci.com/end-of-day-data-search

[4] wsj-us.econoday.com/byshoweventfull.asp?fid=485654&cust=wsj-us&year=2018&lid=0&prev=/byweek.asp#top

[5] www.cnbc.com/2017/12/29/us-stocks-open-higher-sp-500-tracking-for-best-year-since-2013.html

[7] www.cnbc.com/2018/03/29/us-stock-futures-dow-data-tech-and-politics-on-the-agenda.html

[8] www.nytimes.com/2018/03/21/business/fed-interest-rate.html