Articles and Insights

Retirement planning insights, tax strategies, Medicare updates, and lifestyle tips from the TRS team.

Showing 66 of 66 articles

What the Fed's First Rate Cut of 2025 Means for Your Wallet, Mortgages and Investments

The Fed's September 2025 rate cut lowered mortgage rates to 6.26% and could impact savings, CDs, and investments.

September 19, 2025

How the One Big Beautiful Bill Act of 2025 Changes Retirement Taxes

Discover what the new One Big Beautiful Bill Act means for your retirement. Learn about the new senior deduction, estate tax changes, and investment rules.

August 26, 2025Is Your Retirement Plan Ready for the 2025 Tax Law Changes?

Learn how the new 2025 tax law affects retirement income, deductions, and estate planning. Get professional insight and download our free whitepaper.

August 26, 2025

10 Active and Enriching Activities - Winter

Discover fun and safe winter activities for seniors, from cozy indoor hobbies to outdoor adventures, with tips for all mobility levels.

November 26, 2024

The Bucket Planning Strategy: Your Key to a Reliable Retirement Plan

Create a retirement plan with bucket strategy to enjoy worry-free retirement. Watch a free course clip now!

November 22, 2024

From Soldier to Financial Planner: Jim's Journey to Inspiring Others

A former Army interrogator turned financial planner who emphasizes thorough strategic planning and specializes in helping veterans achieve financial security.

November 7, 2024

Navigating Medicare Changes for 2025: What Seniors Should Know

Plan discontinuations, rising out-of-pocket costs, drug coverage shifts, network changes, and reduced supplemental benefits during open enrollment.

October 24, 2024

Ready for Retirement? Find Your Distribution Planner

Learn the difference between accumulation-focused planners and distribution specialists, and why it matters for your retirement income.

October 11, 2024

10 Active and Enriching Activities - Autumn

Ten fall-themed activities including nature walks, pumpkin decorating, baking, crafting, gardening, book clubs, festivals, photography, and more.

September 25, 2024

Summer Experiences: Explore Your Local Farmer's Markets

Farmer's market exploration as community engagement, offering fresh local produce while supporting small-scale agricultural businesses.

August 12, 2024

Do You Need a Trust or a Will? 4 Questions to Ask

Four essential questions to help you decide whether a trust or a will is the right choice for protecting your family and your assets.

August 8, 2024

Your Path to Early Retirement: How To Retire Early

A practical guide to retiring earlier than planned, covering savings targets, lifestyle adjustments, and income strategies.

July 18, 2024

Navigating the Impact of Retirement Age on Benefits: What You Need to Know

How your retirement age affects Social Security, Medicare eligibility, and your overall benefits package.

July 10, 2024

Understanding Retirement Age Trends and Statistics: Insights for Planning Your Future

Data-driven insights into when Americans actually retire, and what the trends mean for your own planning.

July 10, 2024

Embrace Summer: 10 Active and Enriching Activities

Summer activity ideas for retirees looking to stay active, social, and engaged during the warmer months.

June 26, 2024

Strategies for Passing Money Down to Heirs

Smart approaches to transferring wealth to the next generation while minimizing tax impact and protecting your legacy.

June 21, 2024

A Complete Guide to Estate Planning

Everything you need to know about building a comprehensive estate plan that protects your family and your wishes.

June 17, 2024

Estate Planning Basics

A beginner-friendly introduction to estate planning: what it is, why it matters, and where to start.

June 17, 2024

Protecting Your Grandkids' Future: Tips for Saving Money for College

Practical strategies for grandparents looking to contribute to their grandchildren's education fund.

June 17, 2024

Understanding Wills vs Trusts

A clear comparison of wills and trusts to help you make the right estate planning decision for your situation.

June 17, 2024

Flat Fee vs. Commission-Based Financial Advisors

How your advisor gets paid changes the advice you get. Here's how flat fee and commission-based models compare on transparency and trust.

June 10, 2024Navigating the World of Ear Health: Insights from Dr. Hillary R. Perry

A comprehensive guide exploring hearing loss types, hearing aids, tinnitus management, and future hearing technology through insights from audiologist Dr. Hillary R. Perry.

March 7, 2024

Your Social Security Survivor Benefits

Understanding Social Security Survivor benefits (who qualifies, how they're calculated, and how to apply) so your family has support when it's needed most.

February 7, 2024The Electric Car Tax Break You Could Be Missing Out On

A new clean vehicle tax credit can put up to $7,500 back in your pocket when you buy a qualifying EV or fuel cell vehicle in 2023 or later.

October 4, 2023Interesting Facts You Need To Know About Life Insurance

Life insurance still plays a role in retirement, from replacing a spouse's income to covering estate taxes and final expenses. Here's what to consider.

May 3, 2023

Six Rules for Successful Investing with Your Non-Retirement Funds

Explore six essential rules for investing non-retirement funds, including maximizing tax advantages, holding investments long-term, and leveraging capital losses effectively.

July 14, 2021

Why Kayaking Can Be the Perfect Retirement Hobby

Kayaking offers retirees an accessible way to enjoy quality time with spouses or pets, connect with nature, and explore new interests while staying active at their own pace.

June 1, 2021

Six Common Issues That Can Cause Stressful Inheritance Disputes

Estate planning is not fun, but it's essential. Six common issues that cause inheritance disputes, and how proper planning and communication can avoid them.

May 19, 2021

Volunteering in Retirement: How to Give Back

Leaving behind your work life is thrilling yet intimidating for retirees. Volunteering allows you to give back to your community and pursue passion projects while finding fulfillment in your golden years.

April 8, 2021

7 Secrets for a Long and Prosperous Retirement

A long, prosperous retirement depends on far more than your bank balance. Here are seven habits that shape a fulfilling next chapter.

March 10, 2021

How to live within your means without restriction

Learn strategies to live within your means without feeling restricted. Discover practical tips including cutting recurring expenses, repairing money leaks, and setting financial goals.

February 10, 2021Medigap Basics: Everything You Should Know About Medigap

Medigap fills the gaps Medicare leaves behind. Here's what each plan covers, when to enroll, and how to choose the right policy.

October 7, 2020

Medicare Fall Open Enrollment: 7 Things You Didn't Know

When your needs change, Medicare fall open enrollment is the window to adjust your coverage. Here are seven things to know before you do.

September 23, 2020

Nine Social Security Facts You Probably Didn't Know

Anyone who works in the United States pays into Social Security. About 65 million Americans are currently receiving Social Security benefits.

September 10, 2020

Your Plan for Retirement in Tri-Cities, WA: Part 1

Retirement in the Tri-Cities is more than financial planning. Here's why a transition coach matters as much as a balanced portfolio.

August 26, 2020Things Women Should Know About Social Security

Social Security has helped American women for 80+ years. Here's what every woman should know to claim every benefit she's eligible for.

August 26, 2020Your Plan for Retirement in Tri-Cities, WA: Part 2

Now that you've retired in the Tri-Cities, here's a guide to day trips, weekend getaways, and the best of Yakima and Spokane.

August 25, 2020Your Plan for Retirement in Tri-Cities, WA: Part 3

From boating on the Columbia to wine tasting on Red Mountain. A local guide to enjoying the Tri-Cities lifestyle in retirement.

August 24, 2020

Finding Balance and Happiness After Retirement in Denver, CO

You've built a solid retirement plan, but have you considered the mental, physical, social, and spiritual side of life after work?

August 19, 2020

The Denver, CO Hiking Guide for Active Seniors

A guide for active seniors in Colorado on how to safely and confidently enjoy hiking and backpacking in the Denver area and Rocky Mountains.

August 19, 2020

HSA vs. FSA: What's the Difference?

Both accounts are federal government programs designed to help pay for medical expenses that aren't covered by insurance. Here's how HSAs and FSAs differ.

July 29, 2020

Retirement bucket list: 10 Things to do before retirement

Many people have bucket lists of things they want to do before they die. However, it's just as important to make sure that you have some things sorted out before you retire, as well.

June 18, 2020

What to Do with Your Retirement Accounts During an Employment Lapse

When you leave your job, you have several options for managing your retirement accounts. Many of which can put you in a stronger financial situation.

June 3, 2020

Lose Your Job but Not Ready to Retire? Here's What to Do Next

With current market conditions, many Americans are losing their jobs. Here's what we recommend you do to ensure your future financial well-being.

April 22, 2020Retirement Expenses: Top 7 Money Wasters

Even savvy savers can overspend in retirement. Here are seven common money wasters and practical ways to cut them.

March 11, 2020Should You Worry About Your Credit Score in Retirement?

Retiring doesn't directly affect your credit score, but smaller income, big purchases, and lifestyle changes can. Here's how to protect it.

January 29, 2020What Should You Do With Your Old 401(k)?

Leave it, move it, roll it over, or cash it out. A clear breakdown of your four options for handling an old 401(k).

January 2, 2020

Is early retirement right for you? Consider these things first

Before you clock out for the last time and head for Boca Raton, we want to share some important information with you about retiring early.

December 4, 2019Types of Financial Professional Designations and Certifications: What You Should Consider When Selecting an Advisor

A breakdown of the most common financial designations and certifications (CFP, ChFC, CFA, CPA, FRM, FMVA) and how to choose the right advisor.

November 19, 2019

How to Painlessly Downsize Your Lifestyle for Retirement

As you approach retirement, downsizing can reduce housing costs, eliminate time-intensive maintenance, and free up your time, with several other benefits too.

November 6, 2019

Part-Time Jobs in Retirement

Explore part-time job opportunities in retirement to supplement benefits, meet new people, and pursue your passions across various career paths and lifestyles.

October 7, 2019

Best Work-From-Home Jobs for Retirees

Looking for extra income in retirement? Here are the best work-from-home opportunities, from consulting and tutoring to blogging and virtual assistant work.

September 12, 20199 Costly Medicare Mistakes You Can Avoid

Costly Medicare mistakes are avoidable. Here are nine common missteps and how a little research can help you sidestep them.

June 6, 20196 Medicare Facts Every Retiree Should Know

Health care is one of the biggest pieces of retirement planning. Here are six Medicare facts every retiree should know before they enroll.

May 22, 2019The Best Travel Tips for Retirees on a Budget

Travel in retirement can be both rich and affordable. Here are simple tips to stretch your travel budget further on every trip.

May 9, 20196 Strategies to Help Entrepreneurs Save for Retirement

Entrepreneurs face unique retirement challenges without corporate benefits. Here are six strategies (from tax-advantaged accounts to automation) to help you save.

April 23, 2019How to Properly Plan for a Forced Early Retirement

Over half of workers over 50 face a forced early retirement. Here are seven steps to plan now and protect your future income.

April 18, 2019Retirement Budgeting 101: How to Create a Retirement Budget

Developing a retirement budget can help you worry less and have more fun during your golden years. Learn simple steps to creating the ultimate retirement budget.

April 11, 2019How to Recover From a Financial Disaster Without Throwing Your Retirement Off Course

A financial setback doesn't have to derail retirement. Here's a calm, step-by-step path back to a plan that works.

April 3, 20195 Life Events That Impact Your Finances in a Big Way

Marriage, kids, loss, job changes, retirement: five life events that reshape your finances, and how to plan for each.

February 27, 20196 Questions to ask before you retire

Retirement is a big life change! Before you retire, consider these 6 essential questions about spending your time, healthcare, lifestyle costs, income replacement, taxes, and partner compatibility.

February 13, 20197 Ways Your Financial Planner Pays for Themselves

From tax strategy to peace of mind: seven ways a financial planner delivers value that often outweighs the fees.

January 17, 2019Episode 25 – Meet The Retirement Solution Family with COO Carin Sevigny

Meet Carin Sevigny, COO of The Retirement Solution. Carin shares her journey from hospitality to finance and what her role entails.

December 26, 2018

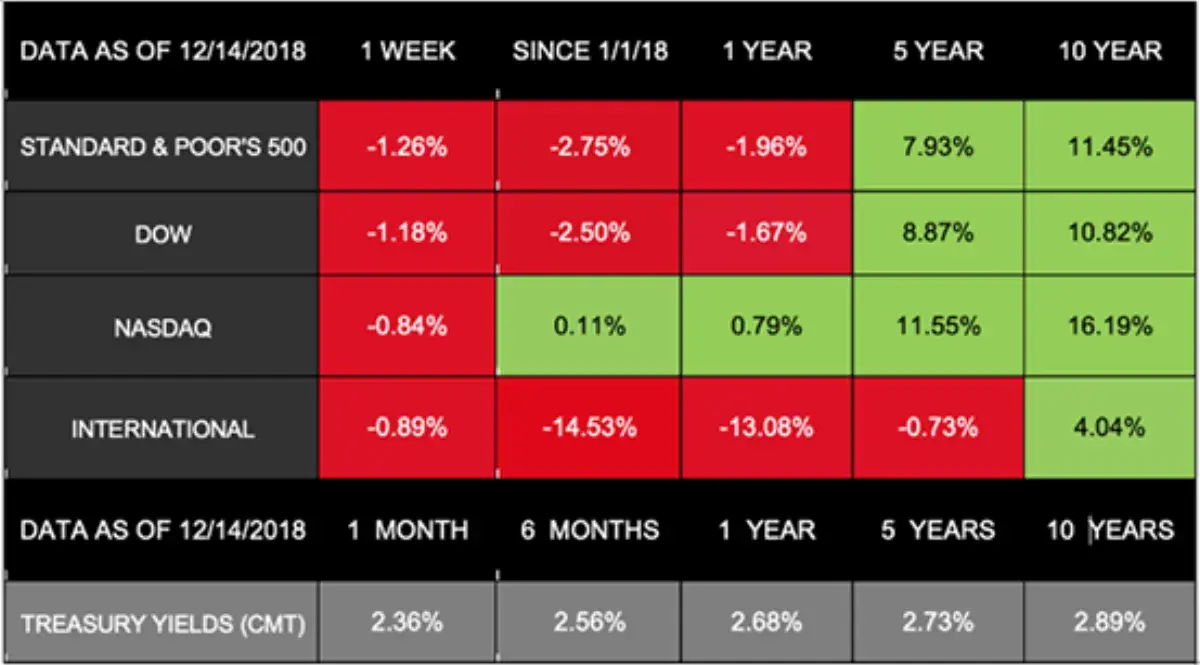

December 17, 2018: Why Did Markets Struggle Last Week?

Last week brought more volatility to the markets, with the S&P 500, Dow, and NASDAQ all ending lower amid global growth concerns.

December 17, 2018How to Help Your Adult Children Without Them Bankrupting Your Retirement

Helping your adult children doesn't have to mean draining your retirement. Here's how to support them with knowledge instead of cash.

December 3, 2018

March 26th, 2018 – Stocks Drop as Tariffs Rise

Markets experienced significant declines last week as trade war concerns triggered by new tariffs on China rattled investors across all major domestic indexes.

March 26, 2018