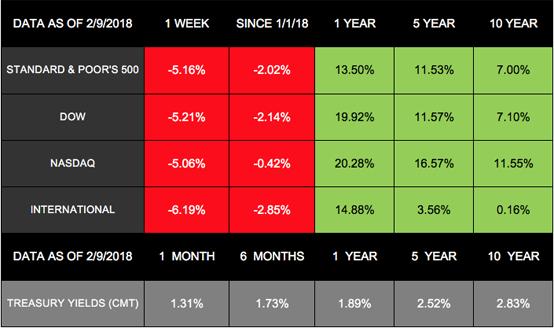

After months of relative calm, market fluctuations are causing many investors to wonder what is happening to the economy. Last week, the S&P 500 lost 5.16%, the Dow dropped 5.21%, and the NASDAQ declined 5.06%.[1] The MSCI EAFE also gave back 6.19%. These losses pushed all four indexes into negative territory for the year. In addition, the weekly performance included significant volatility, as stocks had large fluctuations both within days and from one day to the next. The Dow, for example, lost over 1,000 points twice during the week – and also twice gained over 300 points.[2]

[dt_gap height=”10″ /]During times like these, viewing events in their proper context is imperative. This week, we re going beyond our typical market update in an effort to provide you with clarity and perspective.

[dt_gap height=”10″ /]Our Analysis of the Recent Market Turbulence

The markets started 2018 with the wind in their sails, and investors watched as indexes continued their nearly straight-up trajectory from 2017. Then, after the S&P 500’s best January performance since 1997, stocks took a dive at the beginning of February.[3] On Monday, February 5, the Dow and S&P 500 each lost more than 4%, and the NASDAQ’s drop was nearly as significant.[4] The next day, all 3 indexes posted positive returns.[5] The volatility continued throughout the week. On Friday, February 9, the indexes recovered some of their losses, but each still ended the week down more than 5%.[6]

We understand how unnerving these fluctuations can feel – especially as headlines shout fear-inducing statistics. Our goal is to help you better understand where the markets stand today and how to apply this knowledge to your own financial life.

Putting Performance Into Perspective

When markets post dramatic losses or whipsaw back and forth, many people wonder what causes the turbulence and may assume negative financial data is to blame. However, the recent selloff and volatility don’t have the culprits you might expect.

No negative economic update or geopolitical drama emerged to spur the selloff February 5-6. Instead, emotion-driven investing may have combined with computer-generated trading to fuel the decline. In particular, after the latest labor report showed wage growth picking up more than expected, some investors began to worry about increasing inflation.[7] Higher wages can mean companies have to raise their prices to support their labor costs, a cycle that can cause inflation to grow.[8]

While concerns about inflation and interest rates may be to blame for the market fluctuations, it may not be the only detail to focus on. Another key point is important to remember as an investor: Volatility is normal.

Volatility Facts

- Average Intra-Year Declines: Since 1980, the S&P 500 has experienced an average correction each year of approximately 14%. But in 2017, the markets were unusually calm, fluctuating only 3%.[9] Before this recent decline, the S&P had gone more than 400 days without losing over 5% – its longest span since the 1950s.[10]

Takeaway: Markets fluctuate, and the recent lack of volatility is what’s truly unusual.[dt_gap height=”10″ /] - Percentages vs. Points: Many news articles mention that the Dow’s 1,175 – point drop on February 6 was its highest decline in history.[11] While this statement may be true, it leaves out a key detail: The higher an index goes, the smaller a percentage of its total that each point represents. In other words, 1,175 points doesn’t have the same impact at 25,000 that it does at 10,000.

Takeaway: Focus on percentages, not points, to gain a clearer view of market performance. [dt_gap height=”10″ /] - Recovery From Bad Days: The S&P 500 fell 4.1% on February 5, but within 1 day, the index regained 1.7%.[12] Then, on February 8, the S&P 500 lost another 3.8% but gained back 1.49% the next day.[13]

This performance surpasses historical data. If you analyze the S&P 500’s 15 worst days – where the index lost an average of 8.16% – stocks were still in negative territory 1 day later. However, in 13 instances, stocks were back up within a year by about 21%; they remained in positive territory 5 years later.[14]

Takeaway: Even when stocks lose more ground than they just did, they tend to recover and positive performance usually returns.[dt_gap height=”15″ /]

Remembering the Last Market Correction

In August 2011, the S&P 500 lost 6.66% in one day. At that time, the European debt crisis was in full swing, the U.S. had lost its AAA credit rating, and the financial sector was reeling. Volatility measures indicated that many investors were becoming worried.[15] Facing that situation, impulses to leave the market and avoid further losses could have arisen. As is so often the case, however, staying invested paid off.

Only a year later, the S&P 500 had gained over 25%.[16]

Knowing Where to Go From Here

Over short periods of time, the market trades on fear, anxiety, greed, and emotion. Over the long term, however, economic fundamentals drive the markets.

Thankfully, a variety of data indicates that the economy continues to grow:

- Labor Market: The economy added 200,000 new jobs in January and beat expectations. Average hourly wages also increased, bringing 2.9% growth in the past 12 months – the largest rise since 2008-2009.[17]

- Corporate Earnings: The majority of S&P 500 companies who have reported their 4th quarter results have beaten their earnings estimates.[18]

- Service Sector: The latest reading of the ISM Non-Manufacturing Index (which tracks performance and expectations for service-sector businesses) hit its best level since 2005.[19]

- Consumers: The most recent data indicates that personal income and spending are on the rise.[20]

As investors try to determine whether inflation is on the rise and higher interest rates are imminent, volatility could continue. After last year’s smooth sailing in the markets, these fluctuations may feel harder to withstand. The reality is that equities don’t move in a straight line.

Even if volatility is here to stay, we know that price changes can provide new market opportunities. We agree with the economists at First Trust who assert that, “More economic growth will ultimately be a tailwind for equities, not a headwind.”[21]

We encourage you to focus on your long-term goals, rather than short-term fluctuations. As you do, avoid allowing emotions to derail your plans. We also want you to feel comfortable in your financial journey. If your thoughts on risk have changed, call us so we can help you find the best path forward.

As always, we are here to provide you with clarity, perspective, and support during every market environment. Thank you for the confidence you place in our abilities. We consider it a privilege to be good stewards of the assets you entrust to our care.

[dt_gap height=”10” /]

ECONOMIC CALENDAR

Monday: Treasury Budget

Wednesday: Consumer Price Index, Retail Sales

Thursday: Jobless Claims, Industrial Production, Housing Market Index

Friday: Housing Starts, Import and Export Prices, Consumer Sentiment

[dt_gap height=”20″ /]

[dt_divider style=”thick” /]

Notes: All index returns (except S&P 500) exclude reinvested dividends, and the 5-year and 10-year returns are annualized. The total returns for the S&P 500 assume reinvestment of dividends on the last day of the month. This may account for differences between the index returns published on Morningstar.com and the index returns published elsewhere. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

[dt_divider style=”thick” /]

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Investment advisory services and insurance services are provided through The Retirement Solution Inc., a Registered Investment Advisor.

Any economic and/or performance information cited is historical and not indicative of future results. The Retirement Solution Inc. is an investment advisor registered in each state The Retirement Solution Inc. maintains client relationships.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indices from Europe, Australia, and Southeast Asia.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

These are the views of Platinum Advisor Strategies, LLC, and not necessarily those of the named representative,

Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

By clicking on these links, you will leave our server, as the links are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

http://performance.morningstar.com/Performance/index-c/performance-return.action?t=@CCO

https://www.msci.com/end-of-day-data-search

[2] www.cnbc.com/2018/02/09/us-stock-futures-dow-data-earnings-market-sell-off-and-politics.html

[4] money.cnn.com/2018/02/05/investing/stock-market-today-dow-jones/index.html

[6] www.cnbc.com/2018/02/09/us-stock-futures-dow-data-earnings-market-sell-off-and-politics.html

[7] www.cnbc.com/2018/02/05/why-the-stock-market-plunged-today.html?recirc=taboolainternal

[8] www.theguardian.com/business/2018/feb/02/us-bond-market-rout-fears-trigger-wall-street-sell-off

[9] First Trust, Staying the Course, 12/31/17

[11] www.cnn.com/2018/02/06/us/five-things-february-6-trnd/index.html

[13] www.reuters.com/article/us-usa-stocks/wall-street-plummets-sp-dow-confirm-correction-idUSKBN1FS1UG

www.cnbc.com/2018/02/09/us-stock-futures-dow-data-earnings-market-sell-off-and-politics.html

[14] First Trust, S&P 500 Performance After Its Worst Days, 6/17

[15] First Trust, S&P 500 Performance After Its Worst Days, 6/17

money.cnn.com/2011/08/10/markets/markets_newyork/index.htm?iid=EL

[16] First Trust, S&P 500 Performance After Its Worst Days, 6/17

[17] www.ftportfolios.com/Commentary/EconomicResearch/2018/2/2/nonfarm-payrolls-rose-200,000-in-january

[18] insight.factset.com/sp-500-earnings-season-update-february-2

[21] www.ftportfolios.com/Commentary/EconomicResearch/2018/2/5/new-policies,-new-path