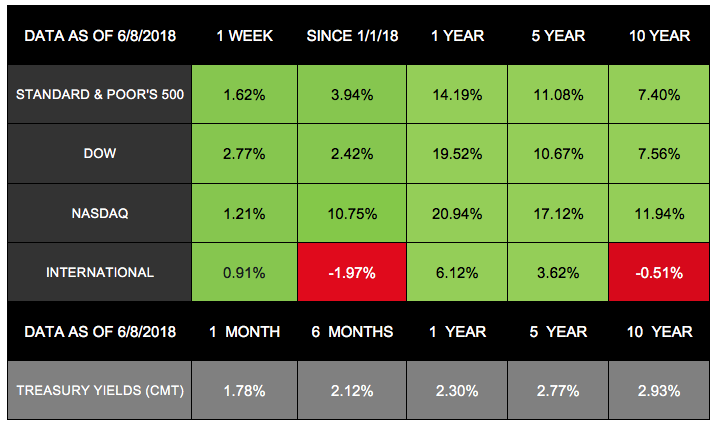

As last week ended, tension between the U.S. and some of its greatest allies was on the rise. Trade remained a hot-button topic ahead of the G-7 meeting in Canada, but investors seemed largely unfazed by the drama.[1] In fact, all 3 domestic indexes posted strong results: The S&P 500 added 1.62% and the NASDAQ gained 1.21%, with both indexes notching their 3rd week of gains in a row.[2] The Dow ended Friday up 2.77% for the week – recording both its highest level and largest weekly gain since March.[3] International stocks were also up, with the MSCI EAFE increasing by 0.91%.[4]

While geopolitical headlines keep unfolding, new data continues to indicate that the U.S. economy is on solid ground. Let’s examine a few updates we received last week:

1. The trade deficit decreased in April.

The latest trade data was largely positive, with the trade deficit hitting a 7-month low and coming in nearly $3 billion lower than expected. In April, exports reached their highest level in history. The economists at First Trust believe that this strong performance could push the 2nd-quarter Gross Domestic Product (GDP) as high as 5%.[5]

2. The labor market continues to tighten.

The latest Job Openings and Labor Market Survey (JOLTS) gave an interesting perspective on our current labor market.[6] Right now, more jobs are available than unemployed people looking for them. Since JOLTS began almost 20 years ago, this has never happened before. The data indicates that employers are struggling to hire people for open jobs – and that the economy is at full employment.[7]

3. The services sector is expanding.

May data from the ISM non-manufacturing index showed that the services sector has experienced its 2nd-best beginning of a year since the index launched in 1997. Business activity and new orders had very positive performance, which could contribute to continuing service-sector growth for the months ahead. The report also showed prices increasing and provided more data that employers are having a hard time filling jobs in this tight labor market.[8]

What is ahead this week?

We will receive two major central bank reports this week – and the historic U.S.-North Korea summit is on the docket as well.

President Trump and North Korea’s leader Kim Jong Un are meeting on Tuesday. The talks should cover North Korea’s nuclear program, but no one can say for sure what market impact it may have.

On a more predictable note, most analysts expect the Federal Reserve to announce its latest interest rate hike on Wednesday. While the markets have likely priced in this increase already, the Fed’s projections for the rest of 2018 could affect investor sentiment.

Meanwhile, on Thursday, experts expect the European Central Bank (ECB) will announce a plan to finally wind down its quantitative easing. If the ECB doesn’t share a timeline for ending this recession-era program, investors may interpret the move as a sign that policymakers are concerned about the EU’s economic outlook.[9]

With a lot to consider this week, we encourage you to remember that many data updates indicate our economy is performing well. As the information unfolds, we’re here to help you separate relevant reports from headline hype. Contact us any time if you have questions about how these details may affect your financial life.

ECONOMIC CALENDAR

Tuesday: Consumer Price Index

Wednesday: FOMC Meeting Announcement

Thursday: Jobless Claims, Retail Sales

Friday: Industrial Production, Consumer Sentiment

[dt_divider style=”thick” /]

Notes: All index returns (except S&P 500) exclude reinvested dividends, and the 5-year and 10-year returns are annualized. The total returns for the S&P 500 assume reinvestment of dividends on the last day of the month. This may account for differences between the index returns published on Morningstar.com and the index returns published elsewhere. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

[dt_divider style=”thick” /]

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Investment advisory services and insurance services are provided through The Retirement Solution Inc., a Registered Investment Advisor.

Any economic and/or performance information cited is historical and not indicative of future results. The Retirement Solution Inc. is an investment advisor registered in each state The Retirement Solution Inc. maintains client relationships.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indices from Europe, Australia, and Southeast Asia.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

These are the views of Platinum Advisor Strategies, LLC, and not necessarily those of the named representative,

Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

By clicking on these links, you will leave our server, as the links are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] www.marketwatch.com/story/dow-futures-slide-130-points-as-g-7-leaders-feud-over-trade-2018-06-08

http://performance.morningstar.com/Performance/index-c/performance-return.action?t=@CCO

www.marketwatch.com/story/dow-futures-slide-130-points-as-g-7-leaders-feud-over-trade-2018-06-08

www.marketwatch.com/story/dow-futures-slide-130-points-as-g-7-leaders-feud-over-trade-2018-06-08

[4] www.msci.com/end-of-day-data-search

[7] wsj-us.econoday.com/byshoweventfull.asp?fid=486198&cust=wsj-us&year=2018&lid=0&prev=/byweek.asp#top