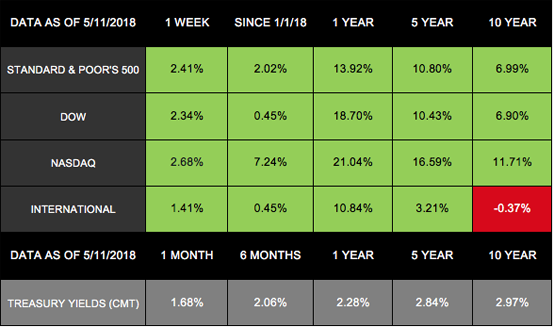

On Friday, the markets closed the week gaining traction. The Dow had 7 days of consecutive growth, rising 2.34% – its largest weekly gain since March.[1]Meanwhile, the S&P 500 rose 2.41%, the NASDAQ jumped 2.68%, and the MSCI EAFE increased 1.41%.[2]

Various factors came together to support the growth. From geopolitical topics to strong corporate earnings, we’ll focus on 3 key developments that drove movement.

1. Energy Shares Boosted by Iran Nuclear Deal Withdrawal

President Trump’s decision on Tuesday to withdraw from the Iran nuclear deal helped push the energy sector higher. With the possibility of renewed sanctions on the horizon, the anticipation of a pullback from global oil supplies helped boost prices. Though oil prices fell from a 3½ – year high on Friday, it was the 2nd week of growth, driving energy shares to rise 3.8%.[3]

2. Technology Sector Jumps Amid Strong Corporate Earnings

After the technology sector’s months of stagnation – fueled in part by recent fears over privacy – it is now approaching all-time highs. Since April 25, the information technology sector has increased 9%. The movement is driving many investors to join the rally, while many analysts remain cautious.[4] Overall, the growth contributed 3.5%.[5]

This rally happened on the back of strong corporate earnings. Over 70% of total S&P 500 companies reported earnings growth that exceeded expectations. Last week’s positive reports helped push the index past 50- and 100-day moving averages.[6]

3. Inflation Remains Steady

The Consumer Price Index (CPI), which measures the price of goods and services, rose only 0.2% for the month in April and 2.5% over the year. These reports both missed and met expectations, respectively.[7] The tepid growth caused some investors to worry that the Federal reserve would raise interest rates more quickly, as the U.S. dollar fell and held below its 2018 high.[8] Some analysts, however, believe that the missed expectations should ease the Fed’s pressure to fast-track interest rates.[9]

Looking Ahead

We will continue tracking geopolitical developments – from potential actions against Syria, tariffs on Iran, and preparations for President Trump’s upcoming meeting with North Korea’s Kim Jong-un.[10] In addition, key discussions around the American Free Trade Act and trade relationships with China remain on the horizon.[11] We also will gain our first insights on how well consumer spending performed in the 2nd quarter.[12]

If you would like to discuss any developments or gain a clearer understanding of how these issues may affect your portfolio, contact us today. We are always here to help you make sense of your financial life and gain clarity for the road ahead.

ECONOMIC CALENDAR

Tuesday: Retail Sales, Housing Market Index

Wednesday: Housing Starts

Thursday: Initial Jobless Claims, Philadelphia Fed Business Outlook Survey, Bloomberg Consumer Comfort Index

[dt_divider style=”thick” /]

Notes: All index returns (except S&P 500) exclude reinvested dividends, and the 5-year and 10-year returns are annualized. The total returns for the S&P 500 assume reinvestment of dividends on the last day of the month. This may account for differences between the index returns published on Morningstar.com and the index returns published elsewhere. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

[dt_divider style=”thick” /]

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Investment advisory services and insurance services are provided through The Retirement Solution Inc., a Registered Investment Advisor.

Any economic and/or performance information cited is historical and not indicative of future results. The Retirement Solution Inc. is an investment advisor registered in each state The Retirement Solution Inc. maintains client relationships.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indices from Europe, Australia, and Southeast Asia.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

These are the views of Platinum Advisor Strategies, LLC, and not necessarily those of the named representative,

Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

By clicking on these links, you will leave our server, as the links are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] www.cnbc.com/2018/05/18/futures-point-to-higher-open-amid-us-china-trade-talks.html

http://performance.morningstar.com/Performance/index-c/performance-return.action?t=@CCO

[3] www.msci.com/end-of-day-data-search

[4] www.nytimes.com/aponline/2018/05/18/world/asia/ap-financial-markets-.html

[6] www.latimes.com/business/la-fi-china-us-trade-war-on-hold-20180520-story.html

[8] www.cnbc.com/2018/05/18/futures-point-to-higher-open-amid-us-china-trade-talks.html

[9] www.latimes.com/business/la-fi-china-us-trade-war-on-hold-20180520-story.html

[11] www.cnbc.com/2018/05/18/us-yields-fall-back-after-climbing-to-fresh-seven-year-peak.html