This Monday, October 9, marks the 10-year anniversary of the S&P 500’s highest point before the Great Recession. While the ensuing decade has provided quite a rocky road for the markets at times, the recovery is undeniable.[1] In fact, last week, markets posted one record high after another – and the S&P 500 had its longest streak of record closes since 1997.[2] At the markets’ close, the S&P 500 added 1.19%, the Dow gained 1.65%, and the NASDAQ grew by 1.45%.[3] International stocks in the MSCI EAFE lost 0.07%.[4]

These domestic gains came despite stocks stumbling slightly on Friday in reaction to disappointing jobs numbers. After 7 years of monthly growth, the September jobs report indicated the first labor market contraction since 2010, with 33,000 jobs lost. The decrease was largely due to the aftermath of Hurricanes Harvey and Irma. Despite this unexpected contraction, however, the unemployment rate fell to its lowest level in 16 years, and average hourly earnings increased by 2.9%.[5]

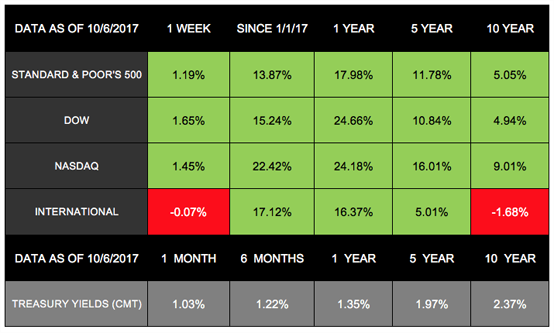

We also began the first trading week of the 4th quarter last Monday, so we will review Q3’s performance and what lies ahead for Q4.

How did the markets perform in Q3?

If we had to pick one word to describe performance in Q3, it would be: positive.

1. Sustained Market Growth

Throughout the quarter, all four indexes we track in this weekly update had solid showings and hit a number of record highs. The S&P 500 was up 3.96%, the Dow rose 4.94%, the NASDAQ jumped 5.79%, and the MSCI-EAFE gained 4.81%.[6] Both the Dow and S&P 500 marked their 8th straight quarter of gains, and the NASDAQ was not far behind with its 5th positive quarter in a row.[7] The S&P 500 even had its least volatile September in over 47 years.[8]

2. Continued Global Gains

Globally, European and emerging markets posted their 3rd straight quarters of impressive gains.[9] In September, Chinese manufacturing experienced its fastest growth since 2012.[10]

What drove the markets in Q3?

Rather than last quarter’s growth rallying around a few sectors, markets advanced broadly in Q3, with 10 of the 11 S&P 500 sectors gaining.[11] This positive performance reflects solid corporate earnings, stronger oil prices, and impressive core capital goods orders – though inflation remained below the Fed’s target of 2%.[12]

What is on the horizon for Q4?

By most accounts, betting against a strong 4th quarter seems like a bad idea: The S&P 500 has grown during Q4 in 7 out of the past 8 years.[13] Americans remain generally bullish on the economy and continue to increase their spending as their incomes grow and inflation remains low.[14]

In addition, manufacturing, services, and housing all seem to be supporting economic expansion.[15] This growth is not limited to the United States; globally, 94% of countries are experiencing year-over-year economic growth.[16]

Of course, the coming weeks will give us an even clearer understanding of Q3 performance – and Q4 expectations. If you have questions about how the markets are affecting your portfolio and future, please let us know. We are here to provide the guidance you need and help clarify your investment process.

ECONOMIC CALENDAR

Monday: Banks Closed for Columbus Day Holiday

Wednesday: JOLTS

Thursday: Jobless Claims

Friday: Consumer Price Index, Retail Sales, Consumer Sentiment

Notes: All index returns (except S&P 500) exclude reinvested dividends, and the 5- year and 10-year returns are annualized. The total returns for the S&P 500 assume reinvestment of dividends on the last day of the month. This may account for differences between the index returns published on Morningstar.com and the index returns published elsewhere. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

Notes: All index returns (except S&P 500) exclude reinvested dividends, and the 5- year and 10-year returns are annualized. The total returns for the S&P 500 assume reinvestment of dividends on the last day of the month. This may account for differences between the index returns published on Morningstar.com and the index returns published elsewhere. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.These are the views of Platinum Advisor Marketing Strategies, LLC, and not necessarily those of the named representative, Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indexes from Europe, Australia and Southeast Asia.

The Dow Jones Corporate Bond Index is a 96-bond index designed to represent the market performance, on a total-return basis, of investment-grade bonds issued by leading U.S. companies. Bonds are equally weighted by maturity cell, industry sector, and the overall index.

The S&P US Investment Grade Corporate Bond Index contains US- and foreign issued investment grade corporate bonds denominated in US dollars. The SPUSCIG launched on April 9, 2013. All information for an index prior to its launch date is back teased, based on the methodology that was in effect on the launch date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology and selection of index constituents in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back tested returns.

The S&P/Case-Shiller Home Price Indices are the leading measures of U.S. residential real estate prices, tracking changes in the value of residential real estate. The index is made up of measures of real estate prices in 20 cities and weighted to produce the index.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Google Finance is the source for any reference to the performance of an index between two specific periods.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

- http://www.investmentnews.com

- https://www.cnbc.com

- http://performance.morningstar.com

http://performance.morningstar.com

http://performance.morningstar.com - https://www.msci.com

- https://www.cnbc.com

- http://performance.morningstar.com

http://performance.morningstar.com

http://performance.morningstar.com

https://www.msci.com - https://www.cnbc.com

- http://money.cnn.com

- http://www.marketwatch.com

- http://www.marketwatch.com

- http://money.cnn.com

https://www.cnbc.com

http://wsj-us.econoday.com - https://www.bloomberg.com

- https://www.bloomberg.com

http://wsj-us.econoday.com - http://wsj-us.econoday.com

- https://www.gsam.com